Welcome to October, which is National Credit Card Awareness month!

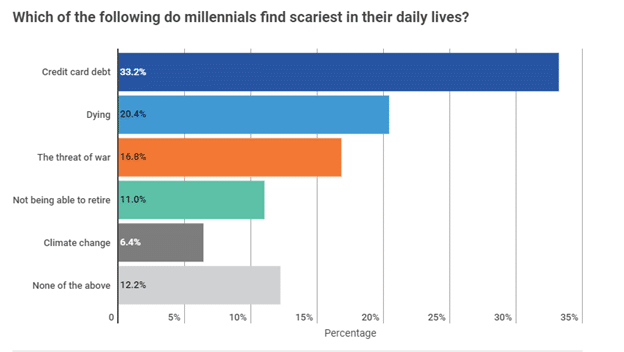

There was an article published on the Credible financial website that did a survey of 500 Americans with credit card debt. The survey said that of those survey participants, age 18-34 years, 33%+ said that debt is the scariest thing in their life. Just over 20% of respondents from this age group identified dying as the next most scary event.

CREDIT CARD DEBT SCARES MILLENNIALS MORE THAN DYING, Y’ALL.

That’s some serious stuff.

Source: https://www.credible.com/blog/millennials-credit-cards-survey/, October 27, 2017

Unfortunately, debt is not uncommon. Three out of every four U.S. millennials have some form of debt (GenForward survey, April 2017). Gen Xers, born between 1965 and 1984, are even worse off; half believe they can’t start saving for retirement until they pay off credit card debt (Study by Allianz Life Insurance Company of North America, 2017). Many bought houses at the top of the market, right before it crashed, so their mortgage debt is extremely high, and sometimes they must live off credit cards to survive.

Ok, so many people under age 50 have a significant amount of debt. So, what can you DO?

Don’t panic. I’m here to help. This blog post will focus on credit card debt, and next time we will focus on student loans. Some of the same suggestions apply.

Know your numbers.

This is kind of like when you are afraid that you might have cancer, so you avoid going to the doctor, and then you finally go, and you should have gone a long time ago because now it’s too late to do anything. You need to step up and look your debt straight in the eye and face it. It’s the only way that it will get better.

Here are numbers you will probably want to get a handle on:

- Your credit score.

- Your debt balances.

- Your interest rates.

Credit Score

Honestly, I think the easiest way to get your credit score is to do what the commercials say: go to creditkarma.com. They will ask you to create an account and ask you questions to prove you are who you say you are. You can see what is impacting your credit score. Credit scores range from 300 to 850. A score of 700 or more is usually considered “good.” If you have a score over 800, you are considered to have “excellent credit.” Why is this important? Because the higher your credit score, the more “credit-worthy” you are. For instance, banks may give you more favorable rates on loans, etc., because they think you are more likely to pay them back.

Debt Balances

You will need to figure out what you owe, and to whom it is owed. So, pull together your credit card statements, or go online and get a login to each credit card website. Once you have the balances, there are many, MANY financial apps that can help you pull all the numbers together.

Interest Rates

You need to figure out what interest rate you are paying on your credit cards, mortgages, student loan, auto, or other type of debts.

Stop Spending.

I call this budget triage. If you truly have a lot of credit card debt, then you need to get real about what you are spending and start cutting. I know, this is like, the WORST part of it. But you can no longer stick your head in the sand. It’s time to start eating more at home. You can start small—if you eat out 5 times a week, maybe cut back to 3 times. I’m not a monster. You may need to call in an accountability partner to help with this (Hint: financial advisor, like myself).

Start Paying everything with cash.

I believe it really does help, psychologically, to pay for things with cash, because then you have money physically leaving your hand, and it might make you think twice about spending it.

Try to get your interest rates down.

If you have good credit, there is a good possibility that you can call your credit card company and simply ask them for a lower rate. I have personally done this. Or you can consolidate cards—put all the debt on your lowest interest rate card, using a balance transfer, or open a new card with a zero percent interest-rate. If nothing else, this will buy you some time to get ahead on interest payments, (if you are not continuing to spend).

Start a side hustle.

If you are already stretched to the bone on spending, consider trying to earn more. There are literally a million things you could do. Start an online business; check out fiverr.com, become a virtual assistant, become a real life personal assistant…etc. Hey, I need someone to cook for me-any takers? 😊 Drive for Uber on the weekends, blog, babysit, whatever, just do it, and put all that extra money towards your debt. Check out this article for ideas.

Use an app to help.

Just Google “apps to help you get out of debt,” and you will find apps that help you track your debt, and give you motivating charts. There are too many to list here, but if you need a recommendation, just email me. Several of them help you figure out the “debt snowball,” which is a term made popular by Dave Ramsey, in which you start by paying off the lowest debt balance first and pay the minimums on all the other cards you have. Then once you pay off that card, you take the payment you WERE making and use it towards the next lowest balance card, etc. The idea is that you build up a payment (like a snowball rolling down a hill, get it?) and eventually pay off everything faster than you would by just paying minimum payments.

Pick a strategy, keep at it and track your progress.

Once you figure out a payment strategy/schedule, it’s important that you stay motivated to keep it going. It can be hard to budget and cut back; find an online group you can join to commiserate with others in the same boat or pick a friend to be your accountability partner.

Don’t stop saving.

You still should ALSO save for retirement and emergencies. I know, it’s hard. You must juggle all these different things, in between working and caring for your kids/pets/self. But you are doing yourself a disservice if you forgo saving for the future, because you should take advantage of compound interest and get started NOW.

If you truly have a lot of debt, you may want to consider a credit counseling organization. They can help you set up next steps. They may also suggest debt consolidation loans or debt settlement, but that should only be a last resort. Check with the National Foundation for Credit Counseling to ensure whomever you work with is legit. Working with a counselor is not the same as working with a private debt-settlement firm that wants to charge you fees upfront. You may want to go the non—profit route with a counselor. Good luck!

Disclosure

*Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. There can be no assurance that the future performance of any specific investment, investment strategy, or product. (Including the investments and/or investment strategies recommended or undertaken by Stephens Consulting, LLC. Doing business as Stephens Wealth Management Group (SWMG). Or any non-investment related content, made reference to directly or indirectly. In this material will be profitable, equal any corresponding indicated historical performance level(s). Be suitable for your portfolio or individual situation or prove successful.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. You should not assume that any discussion or information contained in this material serves as the receipt. Of, or as a substitute for, personalized investment advice from Stephens Consulting.

Please remember that if you are a SWMG client, it remains your responsibility to advise us, in writing, if there are any changes in your personal/financial situation or investment objectives. For the purpose of reviewing/evaluating/revising our previous recommendations and/or services. Or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to your individual situation. You are encouraged to consult with the professional advisor of your choosing.

SWMG is neither a law firm nor a certified public accounting firm and no portion of this article’s content should be construed as legal or accounting advice. A copy of SWMG’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request. Links are being provided for information purposes only. SWMG is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. SWMG is not responsible for the content of any website. Or the collection or use of information regarding any website’s users and/or members. Important Disclosure.

Please Note: Stephens Wealth Management Group does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to SWMG’s website or article or incorporated herein and takes no responsibility for any such content. Such that information is provided solely for convenience purposes only and all users thereof should be guided accordingly.