Market Update

The stock market started off the new year on a positive note following a difficult 2022. After a strong January in the markets, volatility resurfaced in February. Stocks retreated from higher levels with renewed inflation concerns and worries of prolonged interest rate hikes from the Federal Reserve. The S&P 500 ended the first quarter up 7.5%. Technology stocks have performed well so far this year after a challenging 2022. International stocks have been off to a strong start after years of underperforming US stocks. Concerns around the debt ceiling, inflation, future interest rates hikes, and geopolitical tensions have all contributed to the recent volatility. Despite this, the S&P 500 is still up about 18% from the October 2022 market low.

The Federal Reserve raised rates in February and again in March. The Fed had announced earlier this year that interest rates were likely to rise higher than previously anticipated due to recent economic data which had been stronger than expected (including a surprisingly strong labor market). After the recent bank failures, they indicated in March that the interest rate hikes may be nearing an end. The Federal Reserve has now raised interest rates nine times during this most recent rate hike cycle in their efforts to tame inflation (seven times in 2022 and twice in 2023). It can take a year or more for the impacts of interest rate hikes to be felt in the economy. The markets remain focused on whether or not the Fed can fix the inflation problem without causing a serious recession. Inflation is expected to continue to trend downward.

As you know, the recent failure of Silicon Valley Bank (SVB) and Signature Bank has rattled the markets. SVB was heavily concentrated on technology start-ups and venture capital firms. Many of the bank’s clients had deposits above the standard $250,000 FDIC insured limit. As venture funding began slowing down last year, these clients needed to withdraw their cash to pay their bills. In turn, SVB needed to sell investments at a significant loss (longer term bonds which had declined in value due to the Fed’s interest rate hikes) to meet the demand, which caught them off guard. The bank then announced that they were raising capital to replenish their liquidity, which alarmed investors, who then began to withdraw their funds all at once. The FDIC quickly stepped in and took over SVB to stabilize the financial system and protect depositors. They put a plan in place to backstop the full amount of deposits including uninsured deposits over the regular $250,000 maximum. To maintain stability and public confidence in the banking system, the Federal Reserve, Treasury, and FDIC launched a new program (the Bank Term Lending Program) to provide additional funding to banks to ensure that they have the capital to meet the needs of depositors. The recent failure may lead to tighter banking regulation going forward. The Fed may also end up moving more slowly with future rate hikes and possibly end their rate hike cycle sooner than recently expected. This could be a potential positive for both stocks and bonds. While there could be additional banks with issues, the US banking system overall remains well capitalized. We will continue to monitor the situation closely. It should be noted that Raymond James remains in a financially sound position and has among the strongest capital ratios in their industry with double the regulatory requirement considered to be well-capitalized.

Key Takeaways:

- SVB was the second largest bank failure in US history.

- No depositors in FDIC insurance banks will lose any of their deposits, even those above the $250k threshold. The FDIC has guaranteed those deposits for now.

- SVB was too reliant on uninsured deposits and did not manage their own asset portfolio for the current rising rate market. Signature Bank catered to Crypto depositors. Both are outliers. However, it is important to understand the nature of your cash balances in any bank in terms of FDIC coverage.

- Raymond James bank is one of the most conservative banks in the industry. More than 90% of their deposits are at or below the $250k threshold, which is the opposite of where SVB was. To learn more, click here.

- In order to understand how to be sure your bank accounts are covered by FDIC, review the rules here.

- Markets remain unsettled, but this does not alter our overall strategy of diversification or process of aligning our investment approach to your financial plan. If you have any questions, please contact us.

The recent bank failures are a good example of an unexpected event that can surprise the markets (which has happened many times over the course of history). Events like this can sometimes lead to investor panic and the impulse to move out of stocks and bonds. Cash has become a much more appealing place to park funds now while stocks are expected to be volatile. However, markets have historically rebounded after downturns and moving funds to cash can mean missing out on a future recovery. While it’s very important to hold cash for short-term liquidity needs, missing out on a market rebound can make it harder to reach your long-term financial goals.

We expect market volatility to continue in the short-term. The labor market, while still strong, looks to be slowing down. Bonds currently have much more attractive yields than they did a year ago and should likely serve as more of a ballast to portfolios when stocks decline. Downturns in the markets can be unnerving, but they’re part of the investing process and why we stress the importance of having a balanced, well diversified portfolio. –Jason Guenther

7 Tax Essentials for Snowbirds

Snowbirds frequently head to places like Florida, Arizona, or California in the winter months, and come back during the summer months. Before you pack up and fly away, here are some tips to help you figure out the tax side of being a snowbird.

Planning for Retirement – Three Key Principles

We get it. Finances can sometimes feel stressful and complicated. Life is a series of events – some simple, others complex. Retirement is one of the more complex.

That’s why we are dedicating a portion of our newsletter to specifically address some of the most pressing retirement planning related topics and concerns for clients in their 30’s, 40’s, or more than 10 years away from retirement.

Here is one question and three thoughts to keep in mind:

At retirement, your financial life effectively dissolves into one binary question; will your money outlive you or will you outlive your money?

Thoughts:

- Your retirement lifestyle is likely the only financial goal on your list that you cannot borrow money to finance.

- Successful investing is goal focused and planning driven. Your investment portfolio should always be in service of your financial plan, which is in service of your goals. The progression is GOALS ⇒ PLAN ⇒ PORTFOLIO.

- Risk, or at least the primary risk you should be concerned with, can best be defined by asking “is our investment portfolio over the long run, supporting our plan to reach our retirement goals?”

You save money today, so you can pay for the things you want in the future. You also spend money today to pay for your current (and in some cases your past) lifestyle. In this month’s newsletter, we explore ways that Stephens Wealth Management can help create and implement the unique picture of the retirement you want to have and ways to deploy your finances to help get you there.

Our clients who are 10 or more years from retirement often ask their advisor:

Am I on track so far? Have I/we saved as much as I/we should have at this point and how much should I/we be saving?

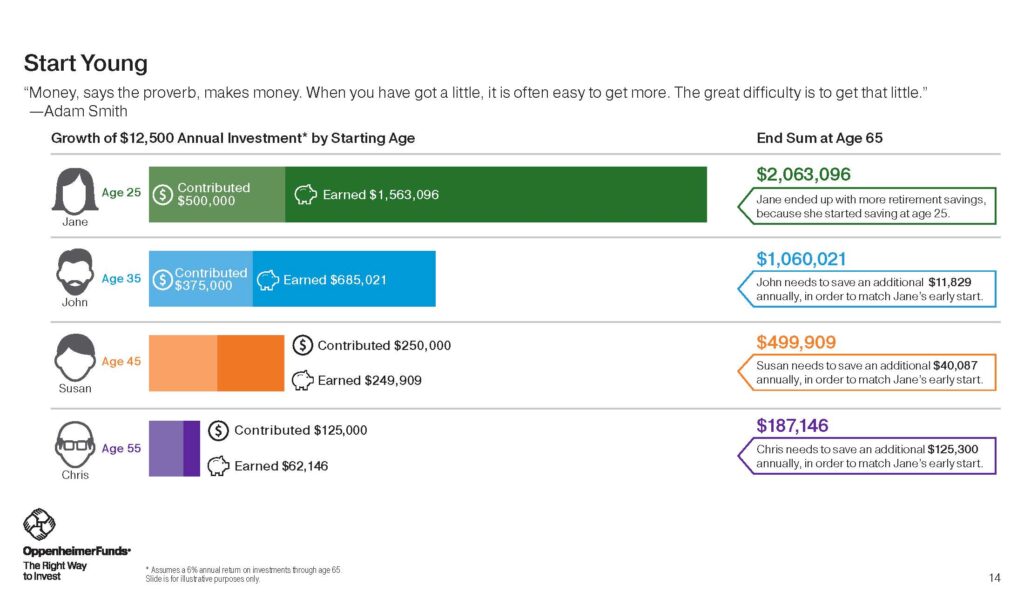

Look at the “Start Young” graphic that depicts the dramatic impact of starting your savings plans early and the high cost of procrastination in either the amount of additional savings needed or the ending values. As Albert Einstein said “Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.”

As you will see it’s worth saving and investing at any age. You can also see the incredible difference it makes, starting sooner rather than later.

How should I/we think about balancing retirement savings, education funding, etc., and still achieving our other financial goals?

With all the competing money priorities in your life, when your next paycheck hits your bank account:

-

- Do you have a plan after you pay all your bills?

- Where should your extra dollars go?

- Do you pay off a credit card balance?

- Do you need to save for an emergency fund, wedding, spend it on home repairs or adopt a pet?

- How do your 401k and other retirement investments fit in?

If these are your questions, please call us and ask about our “Next Best Dollar” tool. The Next Best Dollar tool quickly identifies and steps through each facet of your financial profile to best distribute your money and maximize each dollar you put towards your goals. This analysis helps us collaborate better, allocate your money toward maximizing your net worth, and track your progress of paying off debts, meeting goals, and saving for retirement.

How can we reconcile the different approaches and thoughts my spouse/significant other and I have when it comes to our retirement expectation?

Use “Retirement Bliss,” our financial compatibility tool to see where you and your partner are the same, where you’re different, and get a score that compares you to others (anonymously) like you. It’s a fun way to have a serious discussion about retirement and learn about each other’s vision for the future so you can plan a retirement that is enjoyable and satisfying individually and as a couple.

Many couples retake the quiz year after year to see how they compare. After completing this exercise we’ll have the basis for what is needed to start your retirement plan. Your expectations, concerns, and shared goal inputs can be fed directly into our new financial goal planning tools. To access this tool, please give us a ring.

Our role is to help you – through education, counseling, planning, advice, and implementation. Our intent is to help position your mindset and assets around your current lifestyle while still preparing financially and emotionally for your unique view of retirement. So, as you think about whether it makes sense to spend your own money or secure a loan, how to make changes to improve the probability of success in your retirement plan, or find options that you might like better, we are ready to help.

Women’s Leadership Alliance

As many of our long-term clients know, I am passionate about the field of wealth management and helping women both enter and grow within the field. Did you know that only 16% of wealth advisors are women? I have a personal commitment to work locally with the University of Michigan Flint and have funded a scholarship with the School of Management. I also mentor young female advisors in our industry and across the nation, and serve on the board of the Women’s Leadership Alliance (WLA) to support women entering the wealth management field.

about the field of wealth management and helping women both enter and grow within the field. Did you know that only 16% of wealth advisors are women? I have a personal commitment to work locally with the University of Michigan Flint and have funded a scholarship with the School of Management. I also mentor young female advisors in our industry and across the nation, and serve on the board of the Women’s Leadership Alliance (WLA) to support women entering the wealth management field.

This month I am particularly proud, and a bit emotional, about a tribute that the WLA has put together to recognize the work of my great friend and colleague of nearly 50 years, Judith McGee. She was one of the first women to receive the CFP® certification in the field of wealth management and has provided impactful mentorship and philanthropic stewardship throughout her career. I’ve known Judith since the 1990’s when we met at a Raymond James conference. Over the years, we’ve supported one another in all aspects of running our businesses, working with clients, and our ongoing individual learning and development. When things were tough, Judith was there for me, and she celebrated several successes with me as well.

As a side note, the mission of the WLA, which I helped to found, is to provide education and support for women interested in pursuing a career in the financial planning industry. We concentrate on changing the conversation regarding women and the field of financial advisory services and strive to significantly increase the ranks of women within this dynamic and meaningful profession. –Sherri Stephens

*Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Stephens Consulting, LLC, doing business as Stephens Wealth Management Group (SWMG), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Stephens Consulting. Please remember that if you are a SWMG client, it remains your responsibility to advise us, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, they are encouraged to consult with the professional advisor of his/her choosing. SWMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of SWMG’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request. Links are being provided for information purposes only. SWMG is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. SWMG is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members.

Please Note: Stephens Wealth Management Group does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to SWMG’s website or newsletter or incorporated herein and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users should be guided accordingly.