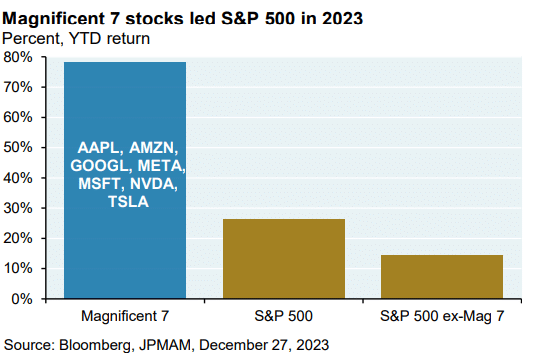

Last year was a surprisingly strong year for the stock market driven by moderating inflation and an AI (artificial intelligence) boom. However, 2023 was really a tale of two markets, with mega cap technology stocks having much stronger performance than the rest of the markets. The S&P 500 was up about 26% for the year.  However, the “magnificent seven” stocks (Apple, Microsoft, Tesla, Nvidia, Amazon, Alphabet and Meta) accounted for over half of the gain in 2023 and about 75% of the stocks in the S&P 500 underperformed the index. See the chart for a visual comparison of the “magnificent seven” performance in 2023 against the S&P 500 with and without these stocks.

However, the “magnificent seven” stocks (Apple, Microsoft, Tesla, Nvidia, Amazon, Alphabet and Meta) accounted for over half of the gain in 2023 and about 75% of the stocks in the S&P 500 underperformed the index. See the chart for a visual comparison of the “magnificent seven” performance in 2023 against the S&P 500 with and without these stocks.

Many economists were forecasting that higher interest rates would push the US economy into recession last year. The economy has remained resilient despite sharply higher borrowing costs as consumers have continued to spend, inflation has cooled, and employers have continued to hire. There’s been much debate as to whether the US will enter a recession in 2024. Alternatively, there could be a series of rolling recessions across different sectors of the economy. In this scenario, certain industries experience a decline whereas the overall economy remains fairly healthy.

The Federal Reserve is likely done with their most aggressive rate hike cycle over the last 40 years. At their last meeting in December, they decided to keep interest rates at their current level and indicated that three rate cuts could be coming this year along with additional ones in 2025. The 10-year US Treasury, which is a benchmark for borrowing costs, hit 5% in October, its highest yield since 2007. Yields declined after the Fed announcement on possible rate cuts and the 10-year US Treasury ended the year near 3.8%. Bonds are now a much more appealing asset class than they’ve been in several years. We believe that now is an attractive time to lock in yields for longer periods of time. Money market funds are still yielding over 5%, but this could come down relatively quick if the Fed were to cut rates over the next year or two. We’ve been talking with clients throughout the past year about ways to earn more attractive yields on cash equivalents including US Treasuries, CDs, and money market mutual funds. There are currently numerous ways to earn over 5% on an annualized basis, which may not be around a year or two from now. Fixed income has struggled over the past couple of years with rising interest rates but could see a boost if the Fed begins cutting interest rates in the future (as bond prices move inversely to rates).

As we look forward, stocks on average have performed well over the twelve months following the Fed’s final rate increase of its cycle. After years of underperformance compared to larger cap stocks, small company stocks have been trading at some of their lowest valuations in recent history. Small cap stocks are typically more sensitive to interest rates and the economy compared to larger companies, so they could see more volatility if we enter an economic slowdown. While we may see more market volatility this year as markets weigh the economic data and implications for Fed policy, we remain cautiously optimistic on the markets over the longer term. We may see some softening in the overall economy in the months ahead and it’s important to maintain a well-diversified and balanced portfolio.

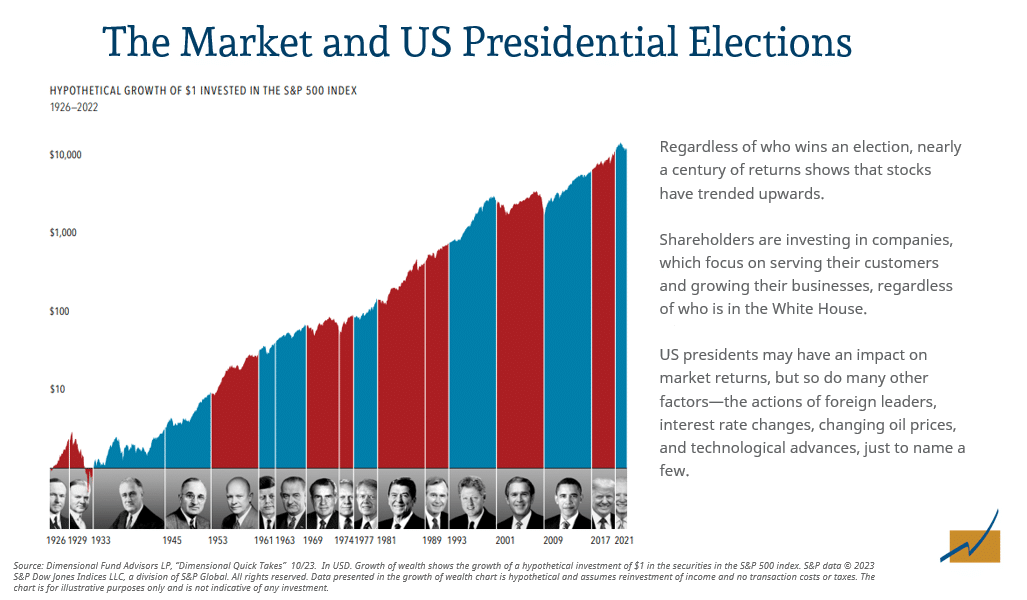

As we enter another election year, it’s important to remember that markets have historically performed well under both parties:

Tax Less Selling

While the opportunities for tax loss selling in 2023 were less than in the previous year, we took tax losses for clients in taxable accounts where it made sense.

2024 Adjustments

The IRS recently increased its tax brackets with inflation adjustments. In addition, for those currently working, the following increases will apply to retirement and health savings account contributions:

| 2024 | |

| 401(k) Contribution | $23,000 |

| 401(k) Catch-up (Age 50+) | $7,500 |

| IRA Contribution | $7,000 |

| IRA Catch-up (Age 50+) | $1,000 |

| Health Savings Account (HSA) Individual | $4,150 |

| Health Savings Account (HSA) Family | $8,300 |

| HSA Catch-Up (Age 55+) | $1,000 |

In addition, the annual QCD (qualified charitable distribution) limit increases for the first time in 2024 to $105,000 from $100,000. This amount will now increase each year with inflation due to the Secure Act 2.0. As a reminder, QCDs allow individuals 70 ½ and older to donate to charities directly from their IRA and have it count towards their RMD (required minimum distribution) and be excluded from taxable income.

*Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Stephens Consulting, LLC, doing business as Stephens Wealth Management Group (SWMG), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Stephens Consulting. Please remember that if you are a SWMG client, it remains your responsibility to advise us, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, they are encouraged to consult with the professional advisor of his/her choosing. SWMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of SWMG’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request. Links are being provided for information purposes only. SWMG is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. SWMG is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Important Disclosure.

Please Note: Stephens Wealth Management Group does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to SWMG’s website or newsletter or incorporated herein and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.