In honor of Financial Literacy month, I’m sharing important information related to credit scores. Do you know what your credit score is? And what it means?

First, shout out to my dad who is turning 69 today. Happy birthday, dad!

Here is the range for Credit Scores:

*Source: https://www.experian.com

You can check your score for free at Creditkarma.com.

So, when I say, a credit score higher than 760 is great, what does that mean? It means that you are likely to get the best possible interest rate when applying for a loan or other form of credit. In addition, the higher your credit score, the more likely you are to be approved for the following:

- Screening for a job

- Renting an apartment

- Applying for insurance

- Getting utilities or cell phone service

When you have a lower credit score, that means that lenders and others will see you as less desirable for renting or extending credit. So if you go to apply for a car loan, you may not get the advertised interest rate—your interest rate could be higher. Landlords may be less willing to rent to someone with a lower credit score as this would alert them to the possibility of a history of late or missing payments, etc.

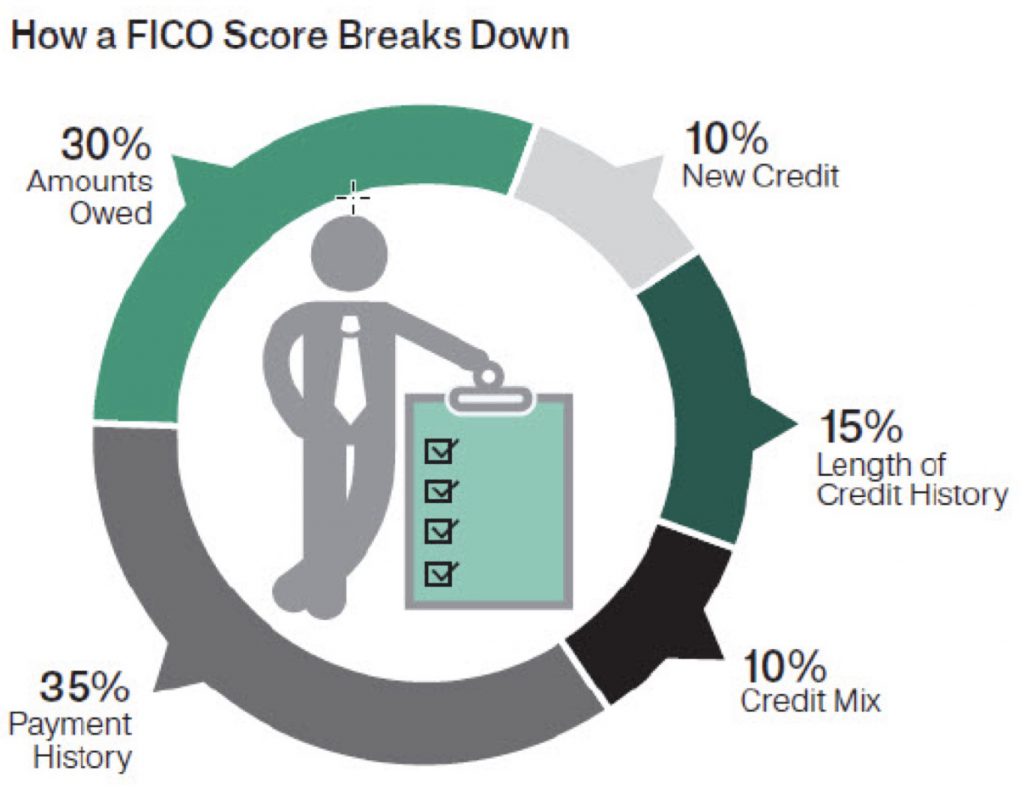

This is what goes into your credit score:

Source: Myfico.com and Bloomberg, 12/31/16.

You can see that if you have a history of not making payments, that will affect your score. The same is true if you don’t have a long credit history or owe quite a bit of debt. These are all factors that will affect your score negatively.

How can you improve your score?

Well, it takes time to improve bad credit, especially if it is due to a bankruptcy or something similar.

However, you can work on improving your score slowly, by doing some or all the following:

- Reviewing your credit report and making sure it is accurate

- Paying your bills on time (not even a few days late)

- Making up missed payments and not missing anymore

- Not opening a lot of new accounts too quickly

- Keeping your credit card balances low

- Paying off debt

- Having fewer credit cards (tip: don’t close unused credit cards if they have no annual fee*.)

*If you close unused cards, your credit card utilization rate may go up (amount of debt you have will be spread among fewer cards; therefore your use per card is higher). So, if the card isn’t charging you a fee, there may be reason to just keep it open. Obviously, if you don’t use a card and it has an annual fee, close it so you aren’t charged that fee each year.

*Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Stephens Consulting, LLC, doing business as Stephens Wealth Management Group (SWMG), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Stephens Consulting. Please remember that if you are a SWMG client, it remains your responsibility to advise us, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to their individual situation, they are encouraged to consult with the professional advisor of their choosing. SWMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of SWMG’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request. Links are being provided for information purposes only. SWMG is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. SWMG is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Important Disclosure.

Please Note: Stephens Wealth Management Group does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to SWMG’s website or newsletter or incorporated herein and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.