So, some people believe that you shouldn’t EVER have debt. I don’t subscribe to this theory. There are times when debt may help. What is the difference between “good” debt and “bad” debt? Well, a simple answer is that good debt helps you finance something that will potentially increase in value, for example, a mortgage. When you buy a house and obtain a mortgage, theoretically, you expect that the house will increase in value. In the future, you could sell and get your money back and then some. Good, right? Plus, the mortgage interest may be tax-deductible, and making payments on time can help you build your credit score. However, if you buy a house that you can’t really afford, or have a really high-interest rate, you may have created bad debt. So, the answer to what is good vs. bad debt is, it depends.

Let’s look at some common forms of debt.

Mortgages/Home Equity Loans:

We already covered first mortgages, but what about taking out a home equity line of credit? Home Equity Lines of Credit (HELOC), allow you to borrow against the equity in your home. This can be a way to free up some cash if you need it, but the interest rates tend to be variable, so they may become higher over time. Sometimes you can be approved for a larger HELOC loan amount, and then you can control the amount of debt you have, by only using what you need. If you need to remodel, pay for college, or consolidate high-interest rate debts, this may be a good option for you. However, there will be closing costs, just like other mortgage debt, and you shouldn’t use this kind of debt to fund your lifestyle, because it still is debt.

Student Loans:

This is typically an example of good debt, because you are financing a degree that you expect to increase your earnings. You are investing in yourself, and student loans may have a low interest rate that may also be tax-deductible. However, it does depend on how much you borrow, what your degree is in, and what you do with that degree. If you get a medical degree and have hundreds of thousands in student loans and then decide to be a drifter for the rest of your life, that would be an example of bad debt.

Business Loans:

If you go into debt because you are trying to finance something in your business that will lead to more income or an asset that you can sell in the future, this could be considered good debt. Plus, the interest on these loans is usually tax-deductible to your business.

Auto Loans:

Experts disagree on whether this is good or bad debt, but many lean towards the “bad” kind. Vehicles are a depreciating asset, so whatever you borrow, you are unlikely to get your money back. Thus, you need to weigh the cost of financing vs. other options. Do you really need a car, or can you get by on public transportation? Maybe you can save up and pay cash for a used car, so you don’t have a loan to pay back. Then, an auto loan might be worth it. Again, it depends.

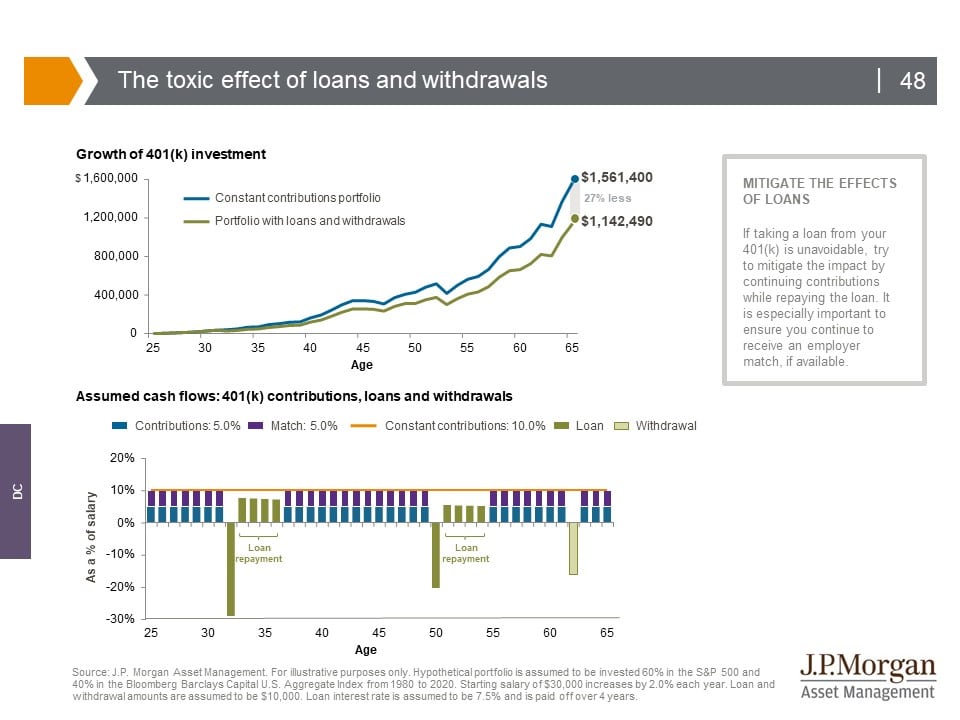

401(k) Loans:

To some, this is almost never a good debt. It *sounds* good, because you are paying yourself back, but the money you loaned yourself is out of the market, and so you are missing out on the compound interest it could be earning. And before you think that is nothing, the chart below shows that it can mean an accumulation of as much as 30% less in your ending balance over time:

Credit Card Debt:

Most of the time, credit card debt is bad debt, in my opinion. The exceptions could be if you know it’s a short-term thing, or you can get a low rate for a set timeframe and then pay off the debt within that timeframe.

Payday Loans/Cash Advance Loans:

These are pretty much the worst kind of debts. The interest rates on these tend to be ridiculously high and you can incur lots of fees. I believe you should avoid these.

With any kind of purchase that may require a loan, it is important to ask yourself, is it worth going into debt to fund this purchase? Will this make my life better or worse in the long-term? My thinking is don’t sacrifice your future to fund the now.

Disclosure

*Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. There can be no assurance that the future performance of any specific investment, investment strategy, or product. (Including the investments and/or investment strategies recommended or undertaken by Stephens Consulting, LLC. Doing business as Stephens Wealth Management Group (SWMG). Or any non-investment related content, made reference to directly or indirectly. In this material will be profitable, equal any corresponding indicated historical performance level(s). Be suitable for your portfolio or individual situation or prove successful.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. You should not assume that any discussion or information contained in this material serves as the receipt. Of, or as a substitute for, personalized investment advice from Stephens Consulting.

Please remember that if you are a SWMG client, it remains your responsibility to advise us, in writing, if there are any changes in your personal/financial situation or investment objectives. For the purpose of reviewing/evaluating/revising our previous recommendations and/or services. Or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to your individual situation. You are encouraged to consult with the professional advisor of your choosing.

SWMG is neither a law firm nor a certified public accounting firm and no portion of this article’s content should be construed as legal or accounting advice. A copy of SWMG’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request. Links are being provided for information purposes only. SWMG is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. SWMG is not responsible for the content of any website. Or the collection or use of information regarding any website’s users and/or members. Important Disclosure.

Please Note: Stephens Wealth Management Group does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to SWMG’s website or article or incorporated herein and takes no responsibility for any such content. Such that information is provided solely for convenience purposes only and all users thereof should be guided accordingly.