Part 1

May is “529” month (get it- 5/29? It’s a complete dad joke). I will be talking about college funding.

Do you have a child or grandchild that will someday attend college? Great, now go back in time and start saving a lot of money about 5 years before they were born, and maybe you will have enough by the time they attend. That’s how it feels these days when considering the cost of college and the savings required.

The cost of college skyrocketed 213% between 1987 & 2017^, so when students take out loans to fund college, that debt can seem overwhelming. But we can help our children by trying to save money before college. There are investment vehicles that can help us do this. In this two-part post, I’m going to talk about several different ways to save:

- 529 plans – Prepaid Tuition Plans

- 529 plans – Education Savings Plans

- Coverdell Education Savings Accounts

- Custodial Accounts

- ABLE Accounts

- Savings Bonds

- Roth IRAs

Some of these have tax advantages, and some don’t. Let’s Jill-splain these. I’ll talk about the first three in this post, and the next 4 in a different post.

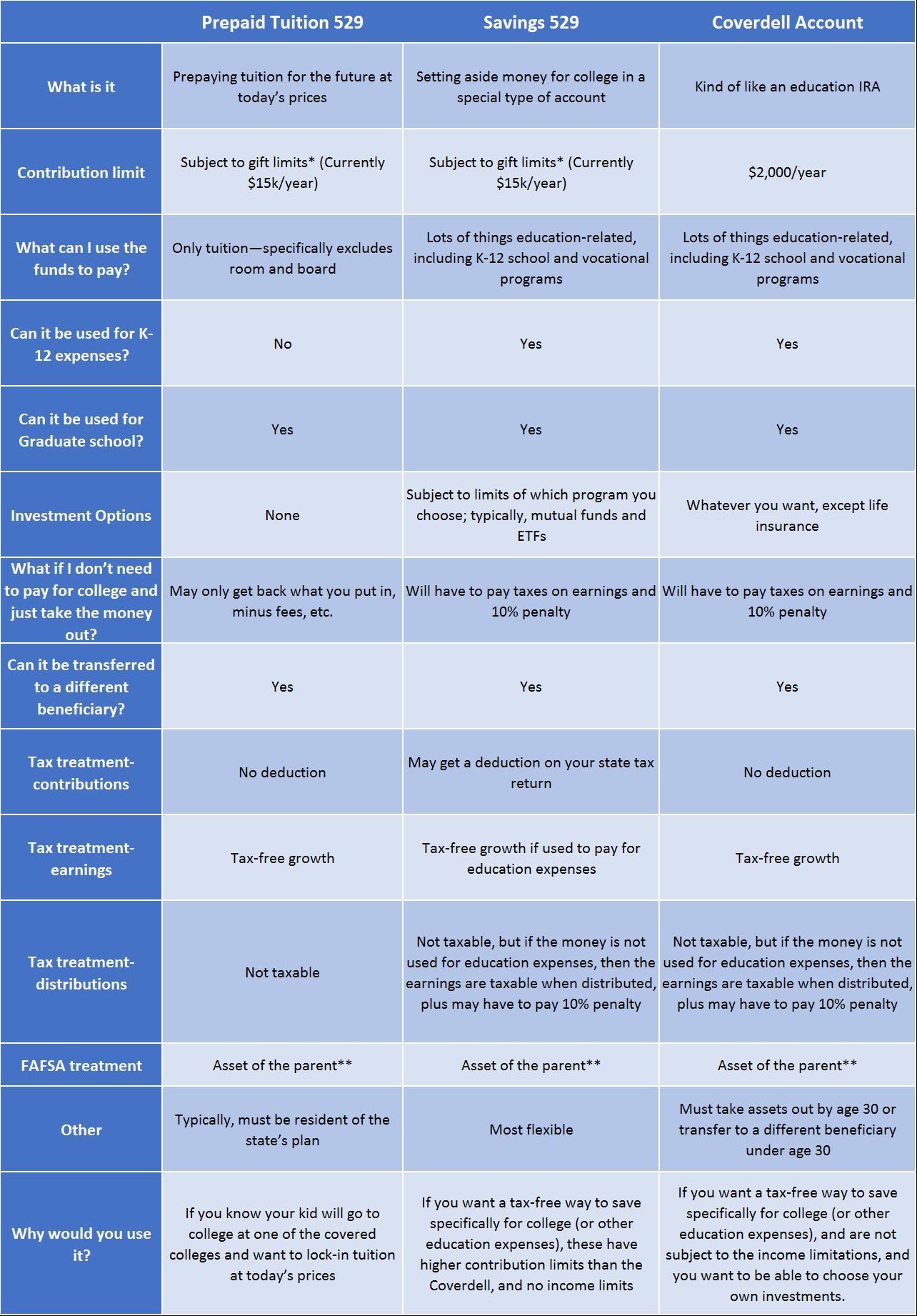

Here is a handy-dandy chart to help:

*529 plans can do what is called “front-loading”, where a parent or grandparent can gift 5 years’ worth of the gifting limit contributions at one time. So, for example, in 2021, a parent could contribute $75,000 to a 529 plan per beneficiary.

**If the parent owns the account, it is treated as a parental asset. But grandparents, aunts, uncles, etc. can also open these types of accounts, and then it is ignored for FAFSA purposes.

^Source: https://www.cnbc.com/2017/11/29/how-much-college-tuition-has-increased-from-1988-to-2018.html

Investors should consider, before investing, whether the investor’s or the designated beneficiary’s home state offers any tax or other benefits that are only available for investment in such state’s 529 savings plan. Such benefits include financial aid, scholarship funds, and protection from creditors.

As with other investments, there are generally fees and expenses associated with participation in a 529 plan. There is also a risk that these plans may lose money or not perform well enough to cover education costs as anticipated. Most states offer their own 529 programs, which may provide advantages and benefits exclusively for their residents. The tax implications can vary significantly from state to state.

Favorable state tax treatment for investing in Section 529 college savings plans may be limited to investments made in plans offered by your home state. Investors should consult a tax advisor about any state tax consequences of an investment in a 529 plan.

*Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Stephens Consulting, LLC, doing business as Stephens Wealth Management Group (SWMG), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Stephens Consulting. Please remember that if you are a SWMG client, it remains your responsibility to advise us, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing.

SWMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of SWMG’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request. Links are being provided for information purposes only. SWMG is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. SWMG is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Important Disclosure.

Please Note: Stephens Wealth Management Group does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to SWMG’s website or newsletter or incorporated herein and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.