Portfolio Rebalancing: What? Why? When?

Have you ever received a Raymond James trade confirmation (or several), and quietly wondered what it was for? It was probably the result of Portfolio Rebalancing, an action I took on your behalf. My name is Jessie Schlanderer, and I am an Investment Analyst and Wealth Advisor here at Stephens Wealth Management Group. In addition to serving on our Investment Committee and advising clients, I am also the primary Portfolio Implementation Manager for the team—that is, the person in charge of trading your accounts once we have analyzed them. As we gear up for summer, I will be rebalancing your portfolios to make sure that they are still on target with your investment goals. Before you receive your influx of trade confirmations, we want to provide you with a little insight into what goes on behind the scenes, as well as a few key reasons why portfolio rebalancing is so important.

Buy Low, Sell High

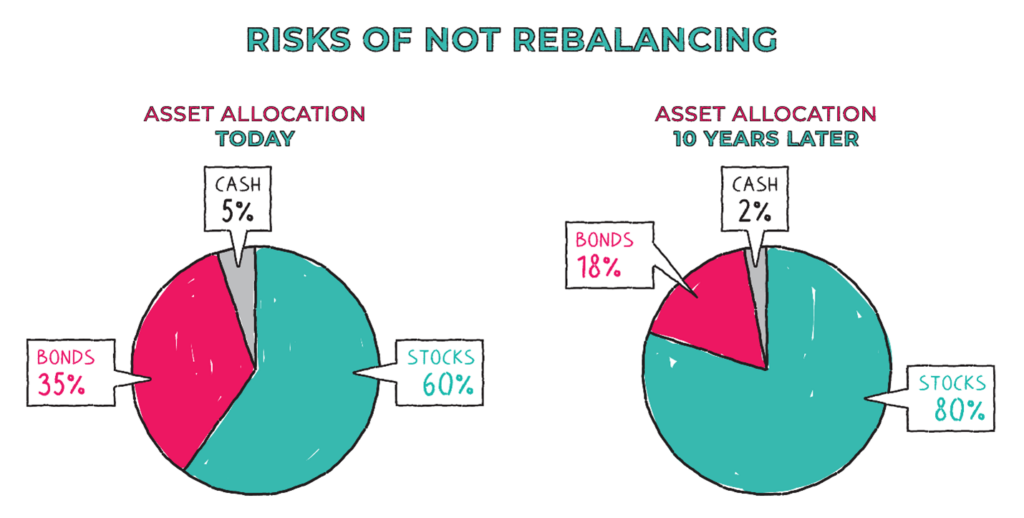

You may have heard this age-old adage—this is the crux of what portfolio rebalancing is all about. As your accounts grow and change, some of your investments will increase in value faster than others. We strive to keep you diversified so that we aren’t trying  to predict which investments will be the short-term “winners,” as that tends to change drastically from year-to-year. As shown in the image to the right from Napkin Finance, after years of compounding, an account that is not regularly rebalanced can look vastly different than what we were originally trying to target, oftentimes transforming your money into a riskier portfolio than you may be comfortable with. To keep you aligned with your goals, we will cut back on some of the funds that have outgrown their position and reallocate that money

to predict which investments will be the short-term “winners,” as that tends to change drastically from year-to-year. As shown in the image to the right from Napkin Finance, after years of compounding, an account that is not regularly rebalanced can look vastly different than what we were originally trying to target, oftentimes transforming your money into a riskier portfolio than you may be comfortable with. To keep you aligned with your goals, we will cut back on some of the funds that have outgrown their position and reallocate that money

to some of the lesser performers—which sounds counterintuitive, but those areas may provide more cushion or potential as the market tide turns. Plus, don’t we all prefer to buy things when they go on sale?

Stay Current with Market Trends

One of the most important components of a long-term investment strategy is to avoid emotional investing—that is, stay the course even when the markets are volatile and avoid trying to “time the market.” With that in mind, our Investment Committee follows and incorporates economic trends to strategically manage your nest eggs while keeping you invested appropriately. We start with a macroeconomic view, looking at opportunities across U.S. versus international stock markets, interest rate and inflation trends, and many other details so that we can navigate these waters on your behalf while maintaining a well-diversified portfolio. As fiduciaries, we also monitor the fund managers that we use and strive to find the best-fit fund to meet our clients’ needs. When we see an opportunity to make a change, we will update our investment strategy and rebalance portfolios to reflect that change. Before you receive your influx of trade confirmations, we want to provide you with a little insight into what goes on behind the scenes, as well as a few key reasons why portfolio rebalancing is so important.

Manage Taxable Gains (and Losses)

The tax management side of rebalancing is two-fold—we try to be prudent when trimming your gains, and harvest losses when we can to help offset those gains. In non-retirement/non-tax qualified accounts, you are required to pay a capital gains tax on any investment growth that you have earned on a position once it is sold (aka realized). When we look to rebalance these “winners” back to target, we review and account for potential capital gains tax. We aren’t always able to avoid capital gains completely (and investment gains, in general, are a positive thing), but we will adjust our trades where possible to minimize your tax liability.

On the other side of that, we also engage in Tax Loss Harvesting—when one of your investments has lost money, we will sometimes sell it to realize the loss. That way, when you have capital gains, these losses can count against the gains to minimize your tax responsibility (you can also carry them forward to use in future years). When we take these losses, we will typically invest the proceeds in something similar for 30 days, and then buy back the original fund. That way you are still invested while making the most of a negative market. This was especially important in a year such as last year when both stock and bond markets were down.

Actively Manage Employer Retirement Accounts

Outside of Raymond James, our team now manages external retirement accounts (such as 401(k) and 403(b) plans) via a platform called Pontera. With this tool, we can manage your retirement account by choosing your investment options, implementing strategies on your behalf, and monitoring changes within your plan, so you can maintain a rebalanced portfolio based on your Investment Policy Statement without having to do the heavy lifting. Rebalancing is a key part of helping us keep these accounts aligned with both our overall investment philosophy and your long-term goals. To learn more about Pontera, or any of our other resources available, please visit our website or reach out to your Advisor. – Jessie Schlanderer

*Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Stephens Consulting, LLC, doing business as Stephens Wealth Management Group (SWMG), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Stephens Consulting. Please remember that if you are a SWMG client, it remains your responsibility to advise us, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to your individual situation, you are encouraged to consult with the professional advisor of your choosing.

SWMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of SWMG’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request. Links are being provided for information purposes only. SWMG is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. SWMG is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Important Disclosure.

Please Note: Stephens Wealth Management Group does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to SWMG’s website or newsletter or incorporated herein and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.