We get it. Finances can sometimes feel stressful and complicated. Life is a series of events – some simple, others complex. Planning for retirement is one of the more complex.

That’s why we are dedicating a portion of our newsletter to specifically address some of the most pressing retirement planning related topics and concerns for anyone in their 30’s, 40’s, or more than 10 years away from retirement.

Here is one question and three thoughts to keep in mind:

At retirement, your financial life effectively dissolves into one binary question; will your money outlive you or will you outlive your money?

Thoughts:

- Your retirement lifestyle is likely the only financial goal on your list that you cannot borrow money to finance.

- Successful investing is goal focused and planning driven. Your investment portfolio should always be in service of your financial plan, which is in service of your goals. The progression is GOALS —> PLAN —> PORTFOLIO.

- Risk, or at least the primary risk you should be concerned with, can best be defined by asking “is our investment portfolio over the long run, supporting our plan to reach our retirement goals?”

You save money today, so you can pay for the things you want in the future. You also spend money today to pay for your current (and in some cases your past) lifestyle. This month, we explore ways that Stephens Wealth Management can help create and implement the unique picture of the retirement you want to have and ways to deploy your finances to help get you there.

Here are some questions that we see people who are 10 or more years from retirement often ask their advisor:

Am I on track so far? Have I/we saved as much as I/we should have at this point and how much should I/we be saving?

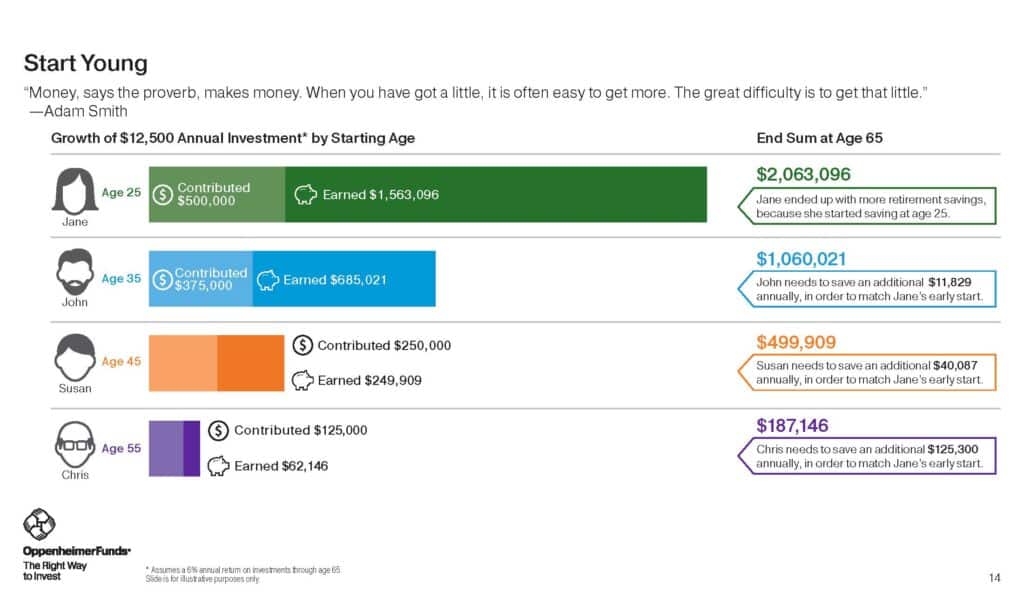

Look at the “Start Young” graphic that depicts the dramatic impact of starting your savings plans early and the high cost of procrastination in either the amount of additional savings needed or the ending values. As Albert Einstein said “Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.”

As you will see it’s worth saving and investing at any age. You can also see the incredible difference it makes, starting sooner rather than later.

Source: Oppenheimer Funds – Assumes a 6% annual return on investments through age 65. The slide is for illustrative purposes only

How should I/we think about balancing retirement savings, education funding, etc., and still achieving our other financial goals?

With all the competing money priorities in your life, when your next paycheck hits your bank account:

- Do you have a plan after you pay all your bills?

- Where should your extra dollars go?

- Do you pay off a credit card balance?

- Do you need to save for an emergency fund, wedding, spend it on home repairs or adopt a pet?

- How do your 401k and other retirement investments fit in?

If these are your questions, please call us and ask about our “Next Best Dollar” tool. The Next Best Dollar tool quickly identifies and steps through each facet of your financial profile to best distribute your money and maximize each dollar you put towards your goals. This analysis helps us collaborate better, allocate your money toward maximizing your net worth, and track your progress of paying off debts, meeting goals, and saving for retirement.

How can we reconcile the different approaches and thoughts my spouse/significant other and I have when it comes to our retirement expectation?

Use “Retirement Bliss,” our financial compatibility tool to see where you and your partner are the same, where you’re different, and get a score that compares you to others (anonymously) like you. It’s a fun way to have a serious discussion about retirement and learn about each other’s vision for the future so you can plan a retirement that is enjoyable and satisfying individually and as a couple.

Many couples retake the quiz year after year to see how they compare. After completing this exercise we’ll have the basis for what is needed to start your retirement plan. Your expectations, concerns, and shared goal inputs can be fed directly into our new financial goal planning tools. To access this tool, please give us a call.

Our role is to help you – through education, counseling, planning, advice, and implementation. Our intent is to help position your mindset and assets around your current lifestyle while still preparing financially and emotionally for your unique view of retirement. So, as you think about whether it makes sense to spend your own money or secure a loan, how to make changes to improve the probability of success in your retirement plan, or find options that you might like better, we are ready to help.

Disclosure

*Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. There can be no assurance that the future performance of any specific investment, investment strategy, or product. (Including the investments and/or investment strategies recommended or undertaken by Stephens Consulting, LLC. Doing business as Stephens Wealth Management Group (SWMG). Or any non-investment related content, made reference to directly or indirectly. In this material will be profitable, equal any corresponding indicated historical performance level(s). Be suitable for your portfolio or individual situation or prove successful.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. You should not assume that any discussion or information contained in this material serves as the receipt. Of, or as a substitute for, personalized investment advice from Stephens Consulting.

Please remember that if you are a SWMG client, it remains your responsibility to advise us, in writing, if there are any changes in your personal/financial situation or investment objectives. For the purpose of reviewing/evaluating/revising our previous recommendations and/or services. Or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to your individual situation. You are encouraged to consult with the professional advisor of your choosing.

SWMG is neither a law firm nor a certified public accounting firm and no portion of this article’s content should be construed as legal or accounting advice. A copy of SWMG’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request. Links are being provided for information purposes only. SWMG is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. SWMG is not responsible for the content of any website. Or the collection or use of information regarding any website’s users and/or members. Important Disclosure.

Please Note: Stephens Wealth Management Group does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to SWMG’s website or article or incorporated herein and takes no responsibility for any such content. Such that information is provided solely for convenience purposes only and all users thereof should be guided accordingly.