September is National Life Insurance Awareness month. So, this month I’ll be posting about life and health insurance. Should you get life or health insurance? Insurance is…. well, sometimes you just must have it. Nobody really says, “yay, I have to buy life or health insurance!”

This blog will cover life and health insurance. There are 2 things I want you to know after reading this:

- The penalty on your tax return for not having health insurance went away in 2019, but…. you still should have health insurance because of the risk to your finances if something bad should happen.

- You only really need life insurance if someone is depending on you for income. If you are single, and don’t have any children, and have money set aside for funeral expenses or someone you know is already going to cover that for you, then you probably don’t need life insurance. But if you do have kids or a spouse/partner or someone that is dependent on you for money and if it would be detrimental to their finances if something happened to you, then you need life insurance.

HEALTH INSURANCE

I’m not going to say much on health insurance. Just know, that it’s complicated. Keeping in mind there are also policies for long term care as well. Additionally, if you have a high‐deductible plan, you can set up a Health Savings Account (HSA) which is a special type of savings account for medical expenses. HSA’s are triple tax‐deferred, making them super awesome because:

- Cash contributions to an HSA are 100% tax deductible (within limits).

- You can earn interest on the cash in the account or in some cases invest part of the cash into investments like mutual funds. Those earnings then grow tax deferred.

- If you withdraw funds for qualified medical expenses, those funds are free from tax.

LIFE INSURANCE

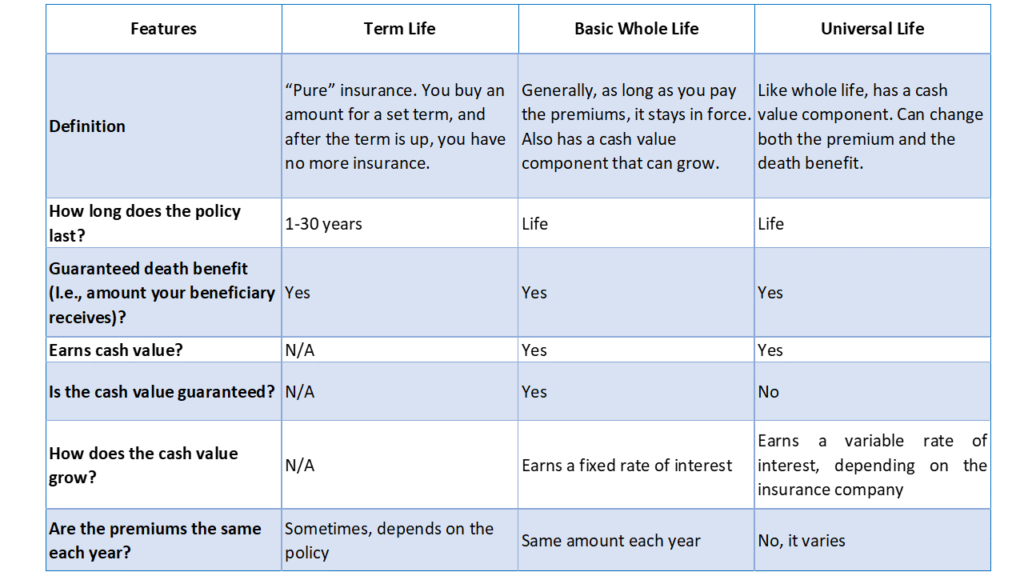

Now, life insurance may also seem complicated. There are different kinds of life insurance, but essentially two main kinds: term and whole life. Term insurance is just that—you buy a policy for a specified term, and then after that, it’s done. If you don’t pass away during that term, then, too bad, nobody gets any money. However, it is also WAY cheaper than the other kind, which is whole life, which can also be known as “permanent” insurance. Whole life is the kind where you buy a policy and you have it until you die if you pay the premiums. And, whole life builds cash value, which can be used to pay premiums, so the policy could essentially “pay for itself” in some cases.

There are also several different types of whole life insurance, such as universal life, variable life, and variable universal life.

Investors should carefully consider the investment objectives, risks, charges and expenses of an investment company product before investing. The prospectus and summary prospectus contains this and other information about investment company products. The prospectus and summary prospectus is available from your financial advisor and should be read carefully before investing.

Be sure you know what you are getting into when buying insurance. What type is right for you, life or health insurance? It depends. A qualified financial professional can help you decide.

*Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Stephens Consulting, LLC, doing business as Stephens Wealth Management Group (SWMG), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Stephens Consulting. Please remember that if you are a SWMG client, it remains your responsibility to advise us, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to your individual situation, you are encouraged to consult with the professional advisor of your choosing.

SWMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of SWMG’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request. Links are being provided for information purposes only. SWMG is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. SWMG is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Important Disclosure.

Please Note: Stephens Wealth Management Group does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to SWMG’s website or newsletter or incorporated herein and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.