You may know that in addition to providing wealth management services to individuals and families, we support business owners with a variety of retirement savings plans for themselves and their employees. These include cash balance, 401(k), and Simple IRA plans. Whether you are a business owner or employee, saving for retirement is important.

Business Owners:

If you do not have a retirement plan in place individually and/or for your employees (or your plan isn’t working as well as you would like), then consider reviewing our webpage dedicated to this topic: Employer Benefit Planning. Note that there are several types of employer plans to consider, and each has different pros and cons. Understandably many people don’t know what questions to ask or where to start in these conversations. We will work with you to identify your goals for the business and for your employer retirement plan. With that and other information about your organization and its employees in mind, we can advise you on the best plan options and aid you in making sound decisions for your future and that of your team. For more information about our retirement planning services for business owners, please reach out at 810-732-7411.

|

2024 Contribution Limits of Note for Business Owners |

|

| Defined Contribution Plan | $69,000 per participant |

| Defined Benefit Plan Contribution | $275,000 maximum annual benefit |

| SEP IRA Contribution | Maximum % of Compensation: 25%

Contribution Limit: $69,000 Minimum Compensation: $750 |

Employees:

Many individuals manage their own work-related retirement accounts, sometimes by choice and often by default. Others have linked their 401(k)s and other work-related retirement savings plans to our online tool, Pontera, allowing us to manage their plans in alignment with risk and growth preferences. Through Pontera we can make changes to investment choices, increase or reduce the amount being invested in each fund, rebalance accounts, etc.

If you are managing your own 401(k) or other employer-provided retirement savings plan, here are some things to think about.

- Review your quarterly statement. Do the contribution numbers and match look correct? How is your account performing over time? If you do not know how to read your statement, ask your plan advisor or your SWMG wealth advisor.

- Ensure you are contributing enough to meet the minimum required for a full employer match. Every company has their own matching schedule.

- Log-in to the plan’s website. Many 401(k) and other retirement plan providers have tools available to support you in your decision making.

- Review the plan’s website to ensure you have account rebalancing set-up. If you aren’t sure what we mean by rebalancing, read this article by wealth advisor Jessie Schlanderer.

- Remember that contribution limits often change year over year. We had an increase in 2024. Individuals can now contribute $23,000, with an additional $7,500 for people aged 50 and over. Note that if you are part of a 403(b)-retirement program, you can contribute an extra $3,000 when you have 15+ years of service.

Did you know that your Health Savings Account (HSA) can serve as a savings account for current and future health care needs? Individuals can contribute up to $4,150 to their HSA per year as of 2024, with an additional $1,000 for individuals age 55+. HSAs offer triple tax benefits if used for qualified medical expenses in retirement. That means your contributions are pre-tax (if made through payroll deductions), and investment growth and withdrawal are also tax free when used for qualified medical expenses. Remember that HSAs are not “use it or lost it” accounts. Money saved in an HSA can remain in the plan indefinitely. An HSA should not be confused with an FSA (Flexible Spending Account), which does have an annual reset in terms of the use of dollars saved. If you choose to use an HSA, note that you can invest some or all the money you put in the account. Again, if you do invest in your HSA account, several of the same tips apply from the 401(k) list above. Our tool, Pontera, can also support the management of your HSA account by your SWMG advisor.

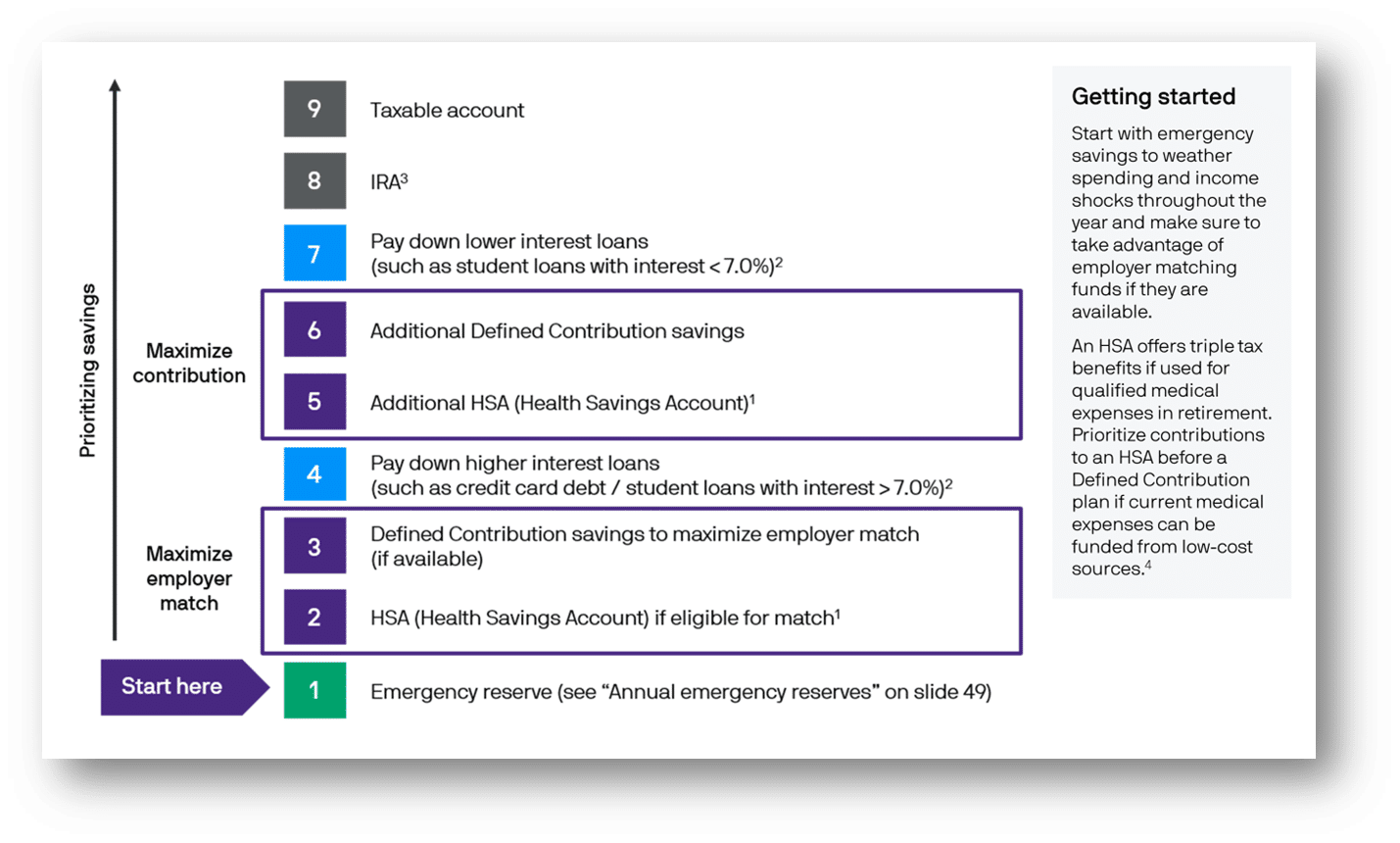

When deciding how much you “should” save and where to save first, we offer the following for your consideration:

Saving for the Future – Step by Step (JP Morgan Guide to Retirement (P. 48, 2023)

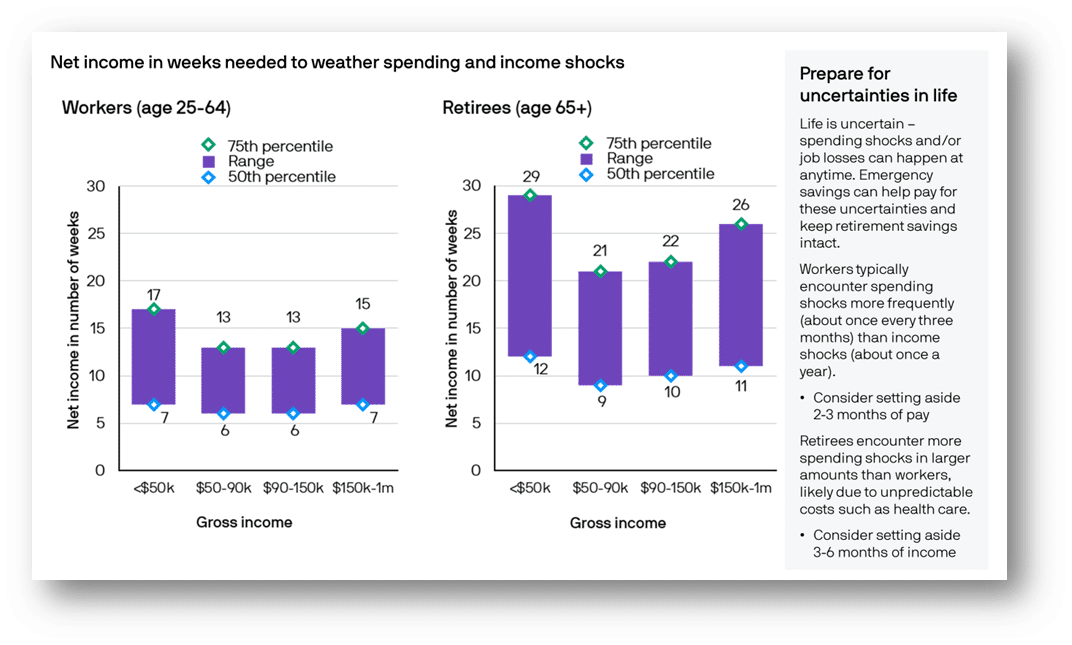

Since step 1 of saving for the future is to ensure you have an emergency reserve, use the following as a resource when determining how much emergency money to save.

Annual Emergency Reserves (JP Morgan Guide to Retirement (P. 48, 2023)

If you have questions about your individual 401(k), HSA, or other employer-offered retirement savings plan, reach out to your wealth advisor.

Disclosure:

*Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Stephens Consulting, LLC, doing business as Stephens Wealth Management Group (SWMG), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Stephens Consulting. Please remember that if you are a SWMG client, it remains your responsibility to advise us, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to their individual situation, they are encouraged to consult with the professional advisor of their choosing. SWMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of SWMG’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request. Links are being provided for information purposes only. SWMG is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. SWMG is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Important Disclosure.

Please Note: Stephens Wealth Management Group does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to SWMG’s website or newsletter or incorporated herein and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.